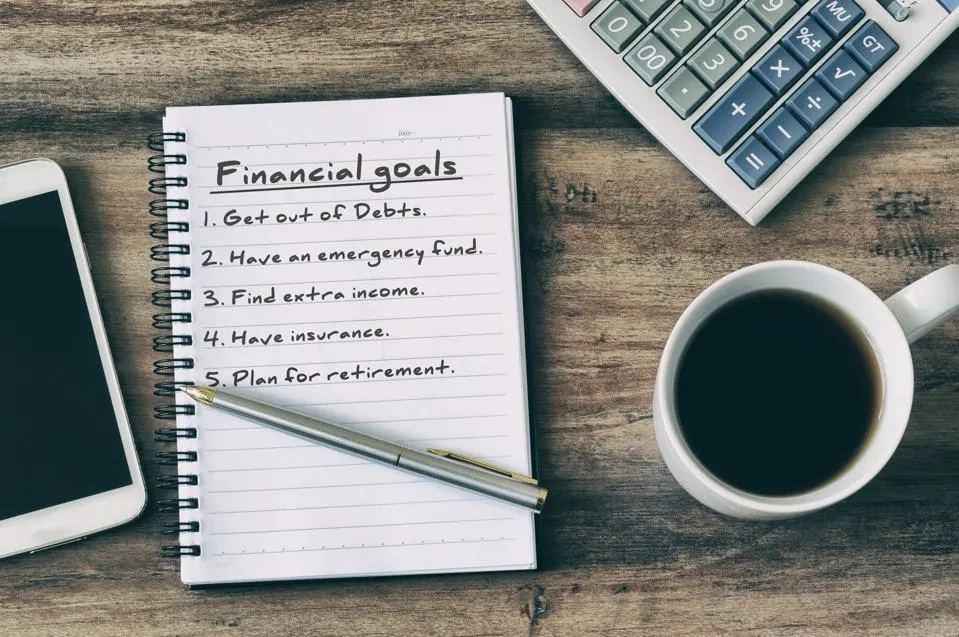

Setting and achieving financial goals is a critical aspect of personal finance management that can lead to greater financial stability and freedom. By identifying specific, measurable, achievable, relevant, and time-bound (SMART) goals, individuals can create a clear roadmap for their financial future. These goals might include saving for a major purchase, building an emergency fund, or planning for retirement. But what strategies can you implement today to ensure that your financial goals are not just dreams but achievable realities?

Here are a few tips to help you set and crush your financial goals.

1. Get Specific

Set specific investment goals that align with your overall financial objectives and determine your risk tolerance. Begin with smaller amounts to gain experience and confidence in the market before scaling up. Use available resources and tools, such as online platforms and mobile apps, which provide intuitive access to trading for beginners. With a clear strategy and a willingness to learn, investing can become a powerful tool in your financial goal-setting toolkit.

2. Track Your Progress

Monitoring progress is absolutely essential to achieving any goal, and financial goals are no exception to this rule. It’s crucial to set up a comprehensive system to track your spending, savings, and investments on a regular basis.

This tracking could be as simple as maintaining a detailed spreadsheet, where you can enter your daily expenses and income, or utilising budgeting apps that automatically sync with your bank accounts and provide real-time updates on your financial status. These tools not only help you visualise your financial habits but also offer insights into areas where you might need to cut back or invest more wisely.

Additionally, setting specific time frames for these reviews—such as weekly or monthly check-ins—can provide a consistent rhythm for evaluating your progress. Regularly reviewing your financial status will not only help you make necessary adjustments to your strategies but will also keep you motivated and accountable on your journey toward reaching your financial aspirations.

3. Be Realistic

When setting financial goals, it’s crucial to take a realistic approach that reflects your current financial situation and abilities. Understanding where you stand financially is key to creating a roadmap that leads to success. While pushing yourself outside of your comfort zone is essential for growth, setting unattainable goals can often result in frustration and discouragement, which may hinder your progress.

Instead, consider starting with smaller, achievable goals that you can build upon. This allows you to gain confidence and experience over time. As you accomplish these initial targets, you can gradually increase the difficulty of your goals, ensuring that they remain challenging yet attainable.

4. Don’t Forget About Emergency Funds

While it’s essential to focus on long-term financial goals, it’s equally crucial not to neglect your short-term needs. Life can be unpredictable, and having a solid financial foundation means preparing for the unexpected. Make sure to set aside funds specifically for emergencies, such as medical expenses, car repairs, or even unexpected job loss.

Having an emergency fund will not only provide you with a safety net but also bring peace of mind, knowing you have resources to fall back on. This financial buffer ensures that you won’t have to dip into your investments or go into debt when unforeseen circumstances arise, allowing you to stay on track with your long-term financial strategies while feeling secure in your day-to-day life.

5. Continuously Re-evaluate and Adjust

As you work towards your financial goals, it’s important to keep reassessing and tweaking your plans. Life keeps changing, and so do your financial needs and priorities. What seemed doable a year ago might not be realistic in your current situation.

Re-evaluating and adjusting your goals as necessary can help keep you on track and avoid frustration or discouragement if things do not go exactly as planned. It also allows you to make the most of new opportunities or changes in circumstances that could positively impact your financial journey.

Conclusion

In conclusion, setting and achieving financial goals requires commitment, discipline, and flexibility. By following these essential tips, you can create a solid financial plan that will help you achieve your dreams and secure your future. Remember to stay focused on your long-term goals while also preparing for the unexpected and continuously re-evaluating and adjusting your plans as needed. With determination and perseverance, you can make significant strides toward financial success.